Insurers need to move from a transactions-driven model to a partnership model, Carnegie-Brown told UK risk managers

The commercial insurance sector is not adapting quickly enough to adjust to the fast-changing needs of its customers, according to Lloyd’s chairman Bruce Carnegie-Brown.

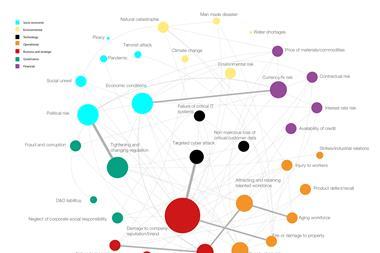

Addressing Airmic’s Leadership Advisory Board earlier this afternoon, Carnegie-Brown said today’s global, interconnected economy provides businesses with a great potential for growth, but at the same time the risk landscape has never been so complex to navigate.

The Lloyd’s market chairman stressed four linked factors driving this complexity:

- Climate change, which appears to be increasing the severity of natural catastrophes and changing the risk profile of previously less impacted regions;

- Urbanisation, which is concentrating high value assets in relatively small areas, making them more vulnerable to systemic shocks;

- Interconnectedness of the global economy, which means that damage in one part of the world can trigger economic consequences in another place;

- Shift in company assets from tangible to intangible, which is making them more vulnerable to digital disruption and to cyber attacks in particular.

“This evolving risk and technological landscape is changing your risk needs,” Carnegie-Brown told the assembled risk managers. “You need new insurance products and services fit for purpose; you need them delivered to you in ways that are efficient, low cost, dynamic, smart and flexible; and you need insurers who can understand and respond quickly to your needs.”

He added that this poses several challenges to insurers: close the innovation gap; adopt new ways of working; embrace new technology; become more efficient; and get closer to their customers.

Carnegie-Brown supported Airmic’s view that the insurance industry needs to shift from a transactions-driven model to a partnership model, within which long-term relationships are established between insurers, brokers and risk managers.

“Today too much of the insurance market is aimed primarily at risk transfer,” he said.

“This is too simplistic for threats such as cyber where the complexity of the risk requires an enterprise-wide response that encompasses emerging risk identification, the quantification of risk appetite in operational risks which are still hard to define, risk mitigation and disaster response planning, and then a determination of which risks an enterprise wishes to retain and which it wishes either to transfer or avoid,” the Lloyd’s market chairman continued.

“Risk managers who are only engaged in insurance buying will be unable to see the whole picture. They need to be full partners in the risk management teams of their employers,” Carnegie-Brown added.

He mentioned the motor insurance market as an example, where the trend is for insurers to have closer connections with customers, which the commercial lines insurance market could learn from.

“Insurers need to move from a competitive model based predominantly on price to one in which value-added services, such as proactive risk advice and prevention, are the differentiating factor, and where advanced data analytics are used to create meaningful customer insights,” Carnegie-Brown said.

“This bespoke approach will help insurers build deeper, longer lasting and higher value relationships with policyholders,” he added.

No comments yet