As climate risks grow more severe, businesses should explore alternative risk transfer solutions, which can help them get back on their feet more quickly following a crisis

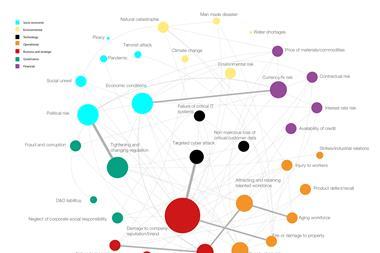

Today’s global risk landscape is increasingly dominated by environmental concerns, particularly those linked to climate change. Recent reports, including the Global Risk Report by the World Economic Forum (WEF), show that the way risk managers are thinking about these threats is changing.

As Nicholas Faull, head of climate & sustainability risk and innovation at Marsh explains: “It’s worth saying that the overall theme of the report was one of declining optimism. You can look at that in terms of the world becoming more risky, more uncertain, and more volatile in general. And a big part of that is the fragmentation of the global order to some degree. So, we’re seeing quite a lot of risks arising from a lack of global coordination.”

Understanding the risks

Organisations are already facing extreme weather events more frequently than ever before. So, the escalation of extreme weather to the number one risk over a ten-year horizon is a significant concern.

The devastation caused by these events is palpable, with recent wildfires in LA, flooding in Valencia, hurricanes across the US, and deadly flooding and landslides in South East Asia serving as stark reminders of the vulnerability not just of businesses but the entire community.

“We’re going to see that evolve,” Faull states, referring to the changing dynamics of global business operations due to climate impacts. “It’s very much seen as not only a short-term risk, but it’s the risk that overwhelmingly becomes critical over the longer term.”

“Adaptation and resilience to extreme weather risks should be a priority - it’s impacting people now. And as action to mitigate climate change continues to move slower than the aspirations of things like the Paris Agreement, it will continue to get worse.”

“The change to the the climate system is going to have an impact on geopolitical and social cohesion risks”

For instance, the intertwining of climate issues with broader geopolitical and social risks could lead to more complex threats. Adverse climatic conditions can exacerbate migration, lead to resource competition, and destabilise regions, while the energy demands of burgeoning technologies, such as AI, further complicate the picture.

Faull comments: “The change to the the climate system is going to have an impact on geopolitical and social cohesion risks as you get greater climate-driven migration over the longer term. I think business and supply chains will see a big impact as different parts of the world become more or less conducive to particular businesses.”

The fragmented nature of the global regulatory framework is another significant challenge. As regions take divergent approaches, businesses face increasing complexity in reporting requirements. This lack of coordination globally could hamper effective climate action and adaptability, and many companies find themselves caught between conflicting regulatory demands, which can lead to inefficiencies and increased vulnerabilities.

Managing the risks

To manage these widespread threats, comprehensive risk management and adaptation strategies are critical. Effective adaptation to extreme weather requires a two-pronged strategy: addressing asset-level vulnerabilities and broader system-level interdependencies.

This means fortifying physical infrastructures while also scrutinising supply chains and community-wide impacts to ensure that contingency measures are in place. Businesses must reinforce supply chains, protecting infrastructure, and understanding the socio-economic fabric that supports their operations.

Faull explains: “Your manufacturing plant is well protected, but if no one can get to work, governments and regulators demand new policies, capital providers increase their requirements, and the resources and that you depend on, like water might are impacted, [then that’s not enough].

He adds: “Awareness is already a step in the right direction,” stressing the importance of understanding dependencies beyond immediate operations. This includes evaluating supply chains for vulnerabilities, especially for critical components sourced from regions prone to climate impacts.

The role of insurance

Insurance is key in managing the repercussions of climate events, creating a financial buffer in times of need, allowing businesses to recover and maintain operations post-disaster. However, it not only serves as financial protection post-disaster but also provides part of the incentive for businesses to invest in resilience measures.

“Insurance really buys an organisation time,” Faull explains. “You have to think about the end-to-end risk life cycle, and risk transfer clearly plays a role. In the event of a loss, it allows a business to get back on its feet and up and running again.”

“Organisations need to understand their evolving risk profile against their current insurances to understand the new and growing drivers of volatility.

However, when it comes to non-damage business interruption, traditional insurance models may fall short. And Faull points to alternative solutions such as parametric insurance as a key part of the answer. This insurance provides cover based on predefined triggers such as quake intensity, water scarcity, temperature, or wind speed – money is paid out quickly and can be used however it is most needed.

Faull concludes: “[Traditional insurance] doesn’t typically cover heat stress events, for example, where there isn’t a property damage trigger. That means that organisations need to understand their evolving risk profile against their current insurances to understand the new and growing drivers of volatility. To help manage these risks alternative insurance mechanisms are going to become more important.”

No comments yet